European Sustainability Reporting Standards (ESRS)

European Sustainability Reporting Standards (ESRS)

Anthesis’ double materiality guide provides a comprehensive overview of the emerging regulatory landscape surrounding double materiality, as well as it’s value and how to conduct a materiality assessment.

The European Sustainability Reporting Standards (ESRS) are a set of reporting standards that are used to meet the requirements of the EU Corporate Sustainability Reporting Directive (CSRD). In other words, whilst the CSRD sets out reporting requirements and obligations, the ESRS provide the framework and methodology for reporting.

The CSRD marks a landmark shift in requirements for companies to report sustainability-related information about their operations, alongside financial information and aims to promote sustainable development through transparency by advancing the scope and quality of corporate sustainability reporting. Implementing the CSRD through the ESRS enables stakeholders to gain improved and comparable insights into the business practices of obligated companies.

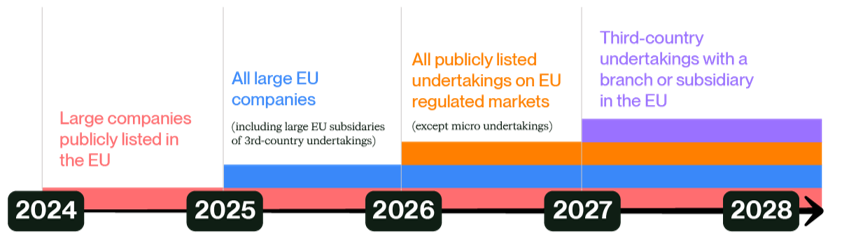

Large, publicly-listed EU companies are required to report in accordance with ESRS for financial years beginning on or after January 1, 2024, and other large companies will be called in for periods on or after January 1, 2025.

The adoption of the CSRD in 2022, and subsequently, the European Sustainability Reporting Standards ESRS in 2023 has continued to show the EU’s ambition to put sustainability reporting at the same level as financial reporting.

Large companies with over 500 employees and who are publicly listed in the EU are required to report in line with the ESRS for financial years beginning on or after January 1, 2024. Other large EU companies have an extra year to prepare, being required to report for periods on or after January 1, 2025.

This second set of large companies consists of those that meet two of the following criteria:

The majority of publicly listed EU undertakings, as well as non-EU companies with branches or subsidiaries in the EU, will then be required to report in 2026 and 2027, respectively.

The CSRD and ESRS represent a critical step forward in the EU’s journey toward a more sustainable business landscape. By harmonising reporting practices and elevating the quality of disclosed information, these initiatives empower stakeholders to make informed decisions, drive positive change, and contribute to a more equitable, sustainable future.

As companies align with these frameworks, they not only comply with regulatory requirements but also position themselves as leaders in sustainability, capable of navigating the complex terrain of ESG considerations with confidence and purpose.

| Approach | Services |

| Set the context – A range of regulations may apply based on your business context, and each carries it own timelines and requirements. | – ESG regulatory landscape evaluation – Product and value chain regulatory scan – Initial team education on requirements |

| Understand what matters – Most current ESG regulations require analysis and reporting based on a type of materiality, up to and including CSRD-compliant double materiality. | – Double materiality assessment – Impact materiality assessment – Financial materiality assessment Risk assessments |

| Identify gaps – Each regulation contains functional and content metrics, requiring in-depth, current state gap analysis. | – Readiness assessments |

| Plan for change – Closing compliance gaps typically means program, governance, and / or disclosure changes on a specific timeline, requiring a custom roadmap and stakeholder alignment. | – Implementation plans |

| Build capabilities – Depending on the regulation, you may need to implement expert-supported projects, such as developing a climate transition plan, to meet your compliance obligations. | – Executive education – ESG governance ESG data management – Transition planning – Scope 1, 2 and 3 GHG inventory – Scenario analysis |

| Report with confidence – Each regulation has specific requirements for assuring and reporting your data, and the higher stakes of financial reporting mean current voluntary reporting should be designed for consistency. | – ESG reporting and assurance support – Voluntary and management standards alignment |

Two cross-cutting ESRSs and ten topic-specific ESRSs (5 environmental, 4 social and 1 on governance) will require disclosure on governance, strategy, and impact, risk and opportunity management.

The cross-cutting ESRS 1 and 2 are mandatory to report on for all obligated companies, whereas the topical standards are only mandatory to report on where material. This is determined through a Double Materiality Assessment, which will support stakeholders in understanding the organisation’s impacts on people and the environment as well as the material financial impacts of sustainability matters on the organisation.

| Group | ESRS Number | Subject |

|---|---|---|

| Cross-cutting | ESRS 1 | General Requirements |

| Cross-cutting | ESRS 2 | General Disclosures |

| Environment | ESRS E1 | Climate |

| Environment | ESRS E2 | Pollution |

| Environment | ESRS E3 | Water and marine resources |

| Environment | ESRS E4 | Biodiversity and ecosystems |

| Environment | ESRS E5 | Resource use and circular economy |

| Social | ESRS S1 | Own workforce |

| Social | ESRS S2 | Workers in the value chain |

| Social | ESRS S3 | Affected communities |

| Social | ESRS S4 | Consumers and end users |

| Governance | ESRS G1 | Business conduct |

There are four reporting areas and three reporting layers that are part of the disclosures.

On July 25, 2024, the EFRAG released a study on the early implementation of the ESRS. The objective of this study was to provide an overview of of emerging practices in the implementation journey of the CSRD and ESRS. The key five takeaways include:

After the standards were first released, they went through a 15-month public consultation process. The basic principles (e.g., double materiality) were retained however, the structure was changed to align more closely with the Task Force on Climate-related Financial Disclosures (TCFD).

Key changes to this iteration of the ESRSs include:

Our services help you navigate today’s regulatory landscape with ease. We guide you in conducting a CSRD-compliant double materiality assessment, identifying data gaps, and planning necessary changes for ESRS compliance.

We build your team’s capabilities to drive positive impact on key topics, ensuring you have the expertise to gather accurate data and report with confidence. With our support, your sustainability reports will be both compliant and meaningful, highlighting your commitment to transparency and responsible business.

Contact us and discover how we can support you to achieve your sustainability ambitions.

We are the world’s leading purpose driven, digitally enabled, science-based activator. And always welcome inquiries and partnerships to drive positive change together.

We’d love to hear from you