EU regulations mandate large companies to report on social and environmental risks and impacts. Is your organisation ready for the Corporate Sustainability Reporting Directive? Find out more about CSRD in the guide below.

The Corporate Sustainability Reporting Directive (CSRD) is the new EU legislation requiring both large and small companies to report on their environmental and social impact activities. It’s being directed by the EU in a bid to help cash flow towards sustainable activities.

In 2021, the European Commission adopted the Sustainable Finance Package, bringing with it one of the proposed measures, CSRD. With CSRD, the European Commission has defined a common reporting framework for non-financial data. Ultimately, it supports stakeholders in evaluating the non-financial performance of organisations. In the long run, it aims to encourage in-scope companies to develop more responsible approaches to business conduct.

As part of the EU Green Deal, the regulation has been developed in response to the challenge that, according to the European Commission, “reports often omit information that investors and other stakeholders think is important”.

CSRD aims to address this challenge, providing a standard reporting framework through which businesses can tie their non-financial reporting.

In 2023, the Corporate Sustainability Reporting Directive (CSRD) was introduced, governing the requirements for sustainability reporting in the EU. The new law marks a significant step up from the existing and relatively limited EU sustainability reporting requirements.

The law will bring sustainability reporting much closer to the discipline and fidelity of financial reporting. The CSRD will significantly impact the data that in-scope organisations need to publish, how that data is collected, and the processes needed to meet the additional requirements of the legislation. The law also required the creation of new European Sustainability Reporting Standards (ESRS) that define the content companies are required to report on.

The CSRD expands the number of companies with activities in the EU to which mandatory sustainability reporting requirements apply. It will inevitably also affect companies outside the EU directly or indirectly through competition and the value chain.

CSRD Implementation Guidance

Find out how to implement the CSRD within your organisation.

On the 10th of November 2022, the European Parliament voted ‘YES’ to the Corporate Sustainability Reporting Directive (CSRD) proposal. Companies are expected to comply with the CSRD standards, starting with the largest listed companies in 2024, other large companies in 2025, and listed small and medium enterprises (SMEs) in 2026. The CSRD is part of the broader ‘European Green Deal’ program that has delivered legislation including the EU Taxonomy Regulation and the Sustainable Finance Disclosure Regulation.

On the 31st of July 2023, the European Commission (EC) adopted the first package of European Sustainability Reporting Standards, including cross-cutting ESRS 1 and ESRS 2, and standards across environmental, social and governance topics. For large EU Public Interest Entities and those already reporting under the Non-Financial Reporting Directive (NFRD), the countdown is now on to report against CSRD for financial years starting on or after the 1st of January 2025.

CSRD Requirements

What information do organisations need to provide to comply with the CSRD standards?

The CSRD reporting requirements outline the following areas to be covered in an organisation’s mandatory sustainability reporting:

Business model and strategy

Sustainability governance and use of sustainability experts

Sustainability policy

Sustainability-related incentives

Due diligence

Value chain data

Impacts, risks and opportunities

Actions, metrics and targets to manage sustainability matters

The ESRS further define the contents and metrics organisations will use to report. The European Commission adopted the first set of ESRS standards in the summer of 2023, and sector-specific standards are now expected in June 2026. In January 2024, new Exposure Drafts of EFRAG’s SME reporting standards were released and will be under consultation until May 2024.

Importantly, companies must report under the double-materiality principle, meaning that sustainability information should consider both the impacts caused by the organisation and the risks and opportunities incurred. This assessment requires the consideration of relevant “sustainability matters” including environmental, social and governance factors.

When reporting, organisations must provide “information necessary to understand the undertaking’s impacts on sustainability matters, and information necessary to understand how sustainability matters affect the undertaking’s development, performance and position.”

Who is Affected by CSRD?

We expect many organisations inside and outside the EU to be affected directly or indirectly.

The legislation directly applies to companies specified by the CSRD. The CSRD requires companies to report on their value chain, so suppliers to CSRD-reporting organisations should expect increased requests and requirements for information.

Specifically, companies in the following categories are required to report under the CSRD and ESRS, given that they meet certain criteria:

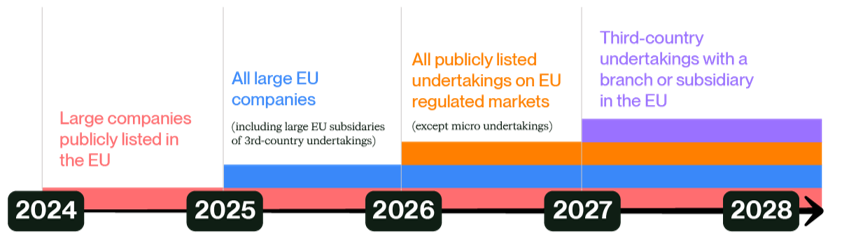

All large undertakings in the EU

All publicly listed undertakings on EU-regulated markets, except micro-undertakings

All undertakings that are parent undertakings of large groups

Third-country undertakings with a subsidiary or a branch in the EU

See the implementation guide for a full breakdown of organisations that are required to report to CSRD:

Timeline for Reporting Sustainability Information (Fiscal Years) – CSRD timeline:

At this point, companies should be aware of the following milestones:

Large, listed companies need to report sustainability information under the CSRD and ESRS for FY 2024 data.

All large companies need to report sustainability information following the CSRD and ESRS for FY 2025 data.

SMEs need to report sustainability information per the CSRD and ESRS for FY 2026 data.

How to Prepare Your Business for the Corporate Sustainability Reporting Directive (CSRD)

Where stakeholder views have previously driven assessment of material issues, EFRAG encourages using data to identify evidence-based impacts, risks and opportunities for an organisation. That said, the views and interests of stakeholders are still fundamental to the identification, assessment and management of material issues.

While there is no prescribed approach for stakeholder engagement as part of CSRD, there is an expectation for companies to engage with stakeholders that may be affected by their activities – from workers across operations and the value chain to communities and consumers. Views and interests of these groups should be collected on an ongoing basis through due diligence practices, with findings pulled into the materiality process where relevant.

To get started, those responsible for compiling their CSRD report should look to engage the following groups:

Investors, business partners and civil society – Companies should consider the perspectives of those who may use the sustainability statement, including these groups, to understand the issues they deem most important.

Finance and risk functions – To corroborate evidence of the materiality of different ESG matters, companies should draw on the expertise of finance and risk functions – not least because the sustainability statement is published alongside the financial statement in the management report, but also as companies are required to assess risks and opportunities for the business from a financial perspective, these functions will need to be involved in setting thresholds for what is to be deemed material.

Auditors – With assurance requirements now a core part of ESG reporting, it is recommended that auditors are involved in the process as early as possible to ensure expectations and methodology are agreed and transparent.

Legal advisors – We also recommend that companies engage with their legal advisors at the beginning of their journey to confirm specific reporting requirements.

The CSRD also prescribes format and process requirements for sustainability reporting. One important requirement is that the reporting shall take place in the management report of the organisation. Another significant change is that the reported information will need to undergo assurance, starting with limited assurance and later to a reasonable assurance standard. These assurance standards are to be developed by the European Commission by 2026 and 2028, respectively.

How Anthesis CSRD Support Can Help You

The introduction of the CSRD arguably marks the most significant change to date in corporate sustainability reporting, and we are here for you to help with the transition. Anthesis CRSD support gives you the information and learning you need, helps you to analyse your needs for change, and supports you in implementing that change.

Anthesis’ approach to CSRD spans six key steps:

Set the context of the regulatory and market landscape that your company sits within

Understand what matters to your organisation in terms of the impacts you cause and those you incur through a CSRD-compliant double materiality assessment

Identify gaps between what information your business already has and what is needed to meet ESRS requirements

Plan for the changes needed to meet data reporting requirements

Build capabilities internally to have more positive impact on your material topics, supported by technical expertise

Report with confidence

Anthesis supports Friends of EFRAG Anthesis is a proud member of “Friends of EFRAG”, demonstrating our commitment to the development of corporate sustainability reporting across Europe, in line with EFRAG’s mission.

CSRD FAQ: Frequently Asked Questions

Currently, around 11,600 companies are required to report sustainability information through the Non-Financial Reporting Directive. However, the introduction of the CSRD means around 49,000 companies in the EU will now have to report non-financial information.

The CSRD applies to all large companies that are established in an EU member state or are governed by EU law, including those who already fall under the NFRD. These companies would include both large and SME public interest entities.

It also applies to all European stock exchange-listed companies (except micro companies) and global businesses that have operations (subject to thresholds) / listed securities on a regulated market in Europe.

The directive defines a large company as one that meets at least two out of three criteria:

€40 million in net turnover;

€20 million total assets on the balance sheet;

250 or more employees.

Yes. Organisations will be required to follow a double materiality process. In short, this means assessing sustainability risks and opportunities affecting the company, as well as its impact on society and the environment.

With the sustainability reporting landscape evolving rapidly, reporting trends are likely to lean towards double materiality in the future, so understanding the impacts from both sides will be vital for accurate reporting.

The CSRD was formally introduced on 1st January 2024. The first cohort required to report are companies already subject to NFRD. They will need to comply with the amended rules, reporting in 2025 for the 2024 financial year.

Other large companies not subject to the NFRD must start reporting from 1st January 2026 on the financial year 2025.

SMEs will not start reporting until 1st January 2027 on the 2026 financial year. However, SMEs are granted the option to voluntarily opt-out until 2028.

For non-European companies that have branches or subsidiaries based in the EU, the new requirements apply from 1st January 2029 for financial year 2028. These companies will have a net turnover of more than €150 million in the EU at consolidated level, and have at least one subsidiary (large or listed) or branch (net turnover of more than €40 million) in the EU.

The CSRD requires companies to report on their value chain, so suppliers to CSRD-reporting organisations should expect increased requests and requirements for information.